Highlights:

- What is a CIBIL Score Rating?

- CIBIL Score Range

- Why does the CIBIL score matter?

- What does a credit report or CIBIL report mean?

- How to Check CIBIL Score Rating?

- Factors that Influence CIBIL Score

- How to additionally foster CIBIL Rating?

- Is it safe to check your CIBIL score online?

The Credit Information Bureau India Limited (CIBIL) is one of the four well-known organizations authorized by the Reserve Bank of India (RBI) to collect credit data. Besides CIBIL, there are three other organizations with RBI authorization, Experian, Equifax and Highmark, who are not as popular. Thus, credit ratings in India are usually referred to directly as the CIBIL TransUnion or simply CIBIL score. Before going further let us understand what a CIBIL score rating is.

What is a CIBIL Score Rating?

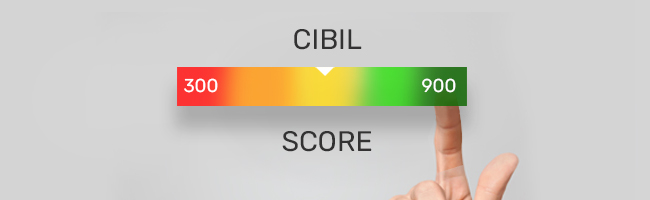

CIBIL score rating is a 3-digit numeric value that reflects your financial record, and it ranges from 300 to 900. The nearer your score is to 900, the better your credit assessment. A CIBIL credit score requires some time to develop. It is estimated that 18 months to 3 years are a sufficient time to develop a good CIBIL score.

The credit score is a reflection of various variables, including the client's instalment history, late instalments, exceptional sums borrowed, etc. Before dismissing or supporting a credit application, moneylenders, banks, and monetary establishments generally take a look at the client's CIBIL score.

A decent CIBIL score mirrors a client's good financial conduct. Individuals with a decent CIBIL score are bound to be supported for credit cards with larger credit limits.

CIBIL Score Range

A CIBIL score goes from 300 - 900, 900 being the top score. Overall, individuals with a CIBIL score of at least 750 are considered trustworthy borrowers. Given below are some CIBIL score ranges.

NA/NH: In case you have no monetary record, your CIBIL score will be NA/NH. This suggests that the borrower is "not suitable" or has “no arrangement of encounters". If you have not used a credit card or have never paid a utility bill in your name, you will have no record as a customer. In such a case you must consider getting a credit card, as it will help you in building a record and a credit history.

300-625: A CIBIL score in this range is considered low CIBIL score. It suggests you have been late in covering credit card bills and EMIs of your existing loans. With a CIBIL score in this range, you may not be able to get a loan or a credit card since CIBIL considers you a defaulter.

625 – 750: A CIBIL score in this range is considered fair. It indicates irregularities in the repayment of your credit. The initial costs on credit cards could be higher on this score but with consistency in payment, you can soon enter a better, more acceptable range.

750 – 800: Assuming your CIBIL score is in this range, you are on your way to building a good credit history. You ought to keep showing great credit conduct and increase your score further. Moneylenders will consider your credit application seriously.

800 – 900: This is an excellent CIBIL score. It proposes that you have been consistent with credit repayments and have a great repayment history. Banks will offer you credit and credit cards at a lower rate of interest since they are assured of repayment.

Also Read: Tips to Maintain Your Business CIBIL Score Above 700

Why Does the CIBIL Score Matter?

The CIBIL score gives an initial evaluation for the bank or the lending institution. The higher the score, the better are your chances of getting your credit endorsed. The choice to loan is exclusively dependent upon the bank or the lending financial institution, and CIBIL does not in any way, choose if the credit/credit card ought to be authorized or not. It only provides the bank or the lending financial institution, with a fair perspective on the repayment ability of the borrower. Thus, the CIBIL score just features as an essential part of the credit application process.

When someone comes to a bank or a financial institution, for credit, the lending institution first checks the prospective borrower’s CIBIL score and CIBIL report. In case the CIBIL score is low, the bank may not consider the application for further processing. If the CIBIL score is high, the bank will evaluate the application and consider various aspects (in addition to the CIBIL score) before approving credit.

What Does a Credit Report or CIBIL Report Mean?

- A credit report or CIBIL report is the record of a borrower's repayment capacity.

- It evaluates the prospective borrower's monetary record from different sources, including banks, credit card associations, combination workplaces, and law-making bodies.

- A borrower’s rating is the result of a mathematical computation applied to credit information.

How to Check CIBIL Score Rating?

Method 2: From the official CIBIL website

One can check the CIBIL score by signing in to the CIBIL site and paying a (nominal) fee.

To check your CIBIL score from the official website, follow these steps:

- Visit the official website of CIBIL at www.cibil.com

- Click on the 'Get Your CIBIL Score' button on the homepage.

- You will be directed to a new page where you will have to provide your personal details like name, email ID, date of birth, gender, and PAN card number.

- Once you have filled in the details, click on the 'Accept and Continue' button.

- You will be directed to the payment page where you will have to pay the required fee to check your CIBIL score.

- After the payment is completed, you will receive a confirmation message on your registered email ID.

- You will then be directed to the CIBIL score page where you can view your score and credit report.

Note: CIBIL charges a fee for checking your credit score and report. You may also be required to provide additional information to verify your identity before you can access your credit report.

Also Read: How to Check, Calculate, and Improve CIBIL Score?

Factors that Influence CIBIL Score

- Irregular Payment History: Irregular instalment payments can lead to a bad score. A new CIBIL investigation (detailed by the Monetary Express) says that 30-day misconduct can lessen your score by 100.

- Credit Use Proportion: If you use more than 30% of credit than you are allowed, at any point of time, it will cut your score down. A higher credit usage shows that you have been overspending and thus may turn into a defaulter.

- Credit inquiries: Each time you apply for an advance or a credit card, the bank or the lending financial institution will check your credit report. This is known as a hard request. Hard requests followed by non-approval of credit lead to a lowering of CIBIL score.

How to Additionally Foster CIBIL Rating?

There are a couple of essential practices that can be followed to further develop one's CIBIL rating:

- Pay your credit instalments regularly.

- Pay by the due date and try to pay in full.

- Avoid multiple hard inquiries.

- Maintain credit use proportion. Do not use more than 30% of your credit.

- Utilize your old credit cards without opening new lines of credit.

- If you open new lines of credit, make sure you use all available lines of credit regularly.

Is it Safe to Check Your CIBIL Score Online?

Yes. It is absolutely safe to check your CIBIL score online. Not only does this give you a regular update regarding your credit history, but it also brings to light any disparities that might have crept into your records. Any disparities can be reported online and should be corrected as soon as possible.

DISCLAIMER:

While care is taken to update the information, products, and services included in or available on our website and related platforms/websites, there may be inadvertent errors or delays in updating the information. The material contained in this website and on associated web pages, is for reference and general information purposes, and the details mentioned in the respective product/service document shall prevail in case of any inconsistency. Users should seek professional advice before acting on the basis of the information contained herein. Please take an informed decision with respect to any product or service after going through the relevant product/service document and applicable terms and conditions. Neither Bajaj Housing Finance Limited nor any of its agents/associates/affiliates shall be liable for any act or omission of the Users relying on the information contained on this website and on associated web pages. In case any inconsistencies are observed, please click on contact information.

Trending Articles

loan+against+property Loan Against Property

[N][T][T][N][T]

Everything You Wanted to Know About Loan Against Property2023-12-16 | 5 Min

tax Tax

[N][T][T][N][T]

Top 5 Tax Benefits and Other Advantages of a Joint Home Loan2024-07-10 | 8 min

home+loan Home Loan

[N][T][T][N][T]

How to Pick the Best Home Loan Tenure that Suits Your Budget2023-06-29 | 5 min

[N][T][T][N][T]

6 Smart Tips to Increase Your Home Loan Eligibility2024-06-27 | 4 min

cibil Cibil

[N][T][T][N][T]

High CIBIL Score Helps Low-Interest Rate Loans2024-06-10 | 5 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Top Benefits of a Loan Against Property Over Collateral-Free Loans2024-01-09 | 4 min

home+loan Home Loan

[N][T][T][N][T]

All About Home Loan Balance Transfers2024-06-04 | 4 mins

home+loan Home Loan

[N][T][T][N][T]

Common Myths About Home Loans: All You Need to Know2024-04-08 | 5 min

[N][T][T][N][T]

Loan Against Property for Doctors: An Essential Checklist2024-05-07 | 2 min

cibil Cibil

[N][T][T][N][T]

Does CIBIL Score Affect Loan Against Property Eligibility?2023-02-15 | 7 min

home+loan Home Loan

[N][T][T][N][T]

How Can NRIs Avail of Home Loans in India2025-03-17 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Step-by-Step Process How to Apply for a Loan Against Property2024-03-05 | 4 Min

home+loan Home Loan

[N][T][T][N][T]

Tips to Get Home Loan with Minimum Down Payment in India2023-07-11 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Understanding EMI: Full Form and Calculation Methods2025-02-24 | 3 min

home+loan Home Loan

[N][T][T][N][T]

A Step-by-Step Guide to Home Loan Balance Transfer Application2024-07-09 | 6 min

tax Tax

[N][T][T][N][T]

Should You Get a Home Loan to Save Your Taxes?2024-02-01 | 3 min

[N][T][T][N][T]

NRI Home Loans: 5 Things to Keep in Mind Before Applying2024-02-15 | 4 min

cibil Cibil

[N][T][T][N][T]

What is CIBIL? Understand How It Works and Its Importance2024-01-31 | 6 min

home+loan Home Loan

[N][T][T][N][T]

Why is the Interest Component Higher in the Initial EMIs of a Home Loan2025-03-07 | 6 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Choose the Right Lender for a Loan Against Property2024-12-23 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Pre-EMI or Full EMI: Understanding Home Loan Repayment Options2025-01-16 |

loan+against+property Loan Against Property

[N][T][T][N][T]

Things You Need to Know Before Applying for a Loan Against Property2024-12-02 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Understanding All the Charges on Your Loan Against Property2024-12-27 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Short vs. Long Loan Against Property Tenure - Which Is Better?2024-05-07 | 4 min

home+loan Home Loan

[N][T][T][N][T]

Factors to Consider Before Applying for a Home Construction Loan2022-12-02 | 5 min

home+loan Home Loan

[N][T][T][N][T]

What Is Home Loan Eligibility and How Is It Calculated2024-07-11 | 6 min

cibil Cibil

[N][T][T][N][T]

Everything You Should Know About Your CIBIL Score2024-02-09 | 7 min

[N][T][T][N][T]

Role of Eligibility Calculator Before Availing a Home Loan2025-04-23 | 6 min

home+loan Home Loan

[N][T][T][N][T]

Stamp Duty and Property Registration Charges in Kerala: A Comprehensive Guide2025-04-11 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

How to Use Loan Against Property EMI Calculator2025-04-23 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Loan Against Property for Business: What You Should Know2025-04-22 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Can You Convert a Loan Against Property into a Home Loan? Here’s What You Need to Know2025-04-22 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Key Documents to Check for a Safe and Transparent Property Transaction2025-04-22 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Home Loan Tax Benefits: Is There a Limit on How Many Times You Can Claim?2025-04-22 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

What to Know Before Availing of a Loan Against Property2025-04-22 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

What Happens When You Pay Off Your Mortgage?2025-04-22 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

How to Pay MCD Property Tax in Delhi2025-04-21 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Tax Benefits on Mortgage Loans: What You Need to Know2025-04-21 | 3 min

home+loan Home Loan

[N][T][T][N][T]

How to Apply for GPRA Accommodation via eSampada and eAwas2025-04-21 | 2 min

home+loan Home Loan

[N][T][T][N][T]

Understanding the SVAMITVA Scheme: A New Era of Property Ownership in Rural India2025-04-21 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Why Property is More Than Just an Asset: 4 Ways It Can Power Your Finances2025-04-21 | 2 min

[N][T][T][N][T]

Home Loan Insurance Benefits for New Home Buyers2025-04-21 | 6 min

home+loan Home Loan

[N][T][T][N][T]

MPIGR Madhya Pradesh: A Guide to Property Registration and SAMPADA Services2025-04-14 | 2 min

home+loan Home Loan

[N][T][T][N][T]

Consider These Factors Before Foreclosing Your Home Loan2024-04-16 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Top Things to Keep Track of While Doing a Home Loan Balance Transfer2022-12-18 | 7 min

home+loan Home Loan

[N][T][T][N][T]

Smart Things to Consider Before You Apply for a Home Loan2022-12-14 | 5 min

tax Tax

[N][T][T][N][T]

How Much Tax Can be Saved Under Sections 80C, 80D, and 80G?2024-05-15 | 5 min

tax Tax

[N][T][T][N][T]

Tax Benefits on Home Loans for Self-Employed Individuals: What You Need to Know2024-06-07 | 4 min

cibil Cibil

[N][T][T][N][T]

How to Increase Your CIBIL Score Above 800: 7 Proven Methods2023-01-24 | 4 min

home+loan Home Loan

[N][T][T][N][T]

10 Smart Steps for Effective Home Loan Management2024-02-16 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Should You Take a Home Loan Even If You Have Enough Money to Buy a House?2024-01-30 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Section 80EE: Claim Deductions on the Home Loan Interest Paid2024-04-25 | 6 min

cibil Cibil

[N][T][T][N][T]

How can I Remove Loan Inquiry from CIBIL Credit Report2024-01-22 | 5 min

[N][T][T][N][T]

Tips to Manage Loan Against Property Repayments Efficiently2024-02-21 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Differences Between Fixed and Floating Interest Rates2024-05-15 | 2 min

home+loan Home Loan

[N][T][T][N][T]

What Do You Need to Know About Home Loan Foreclosure?2023-03-23 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Monthly Reducing Balance Method for Home Loan Interest2025-02-25 | 3 min

[N][T][T][N][T]

Everything You Need to Know About Home Loan Part-Prepayment2024-12-18 | 5 min

home+loan Home Loan

[N][T][T][N][T]

What is the Ideal Age to Buy a House?2025-03-19 | 2 min

home+loan Home Loan

[N][T][T][N][T]

Complete Guide to Securing a Attractive Interest on Home Loans2024-01-23 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Check Housing Loan Eligibility with Home Loan Eligibility Calculator2023-07-12 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Everything You Need to Know About Top-up Loans on a Home Loan2024-04-09 | 6 min

home+loan Home Loan

[N][T][T][N][T]

Get a Home Loan Without Visiting Branch: A Step-by-Step Guide2024-03-20 | 4 min

cibil Cibil

[N][T][T][N][T]

Impact of Late Payment on CIBIL Score?2024-03-08 | 6 min

home+loan Home Loan

[N][T][T][N][T]

Home Loan Balance Transfer: Benefits, Eligibility, and More2024-05-15 | 3 Min

[N][T][T][N][T]

7 Benefits of Taking a Home Loan in India2024-06-19 | 3 min

home+loan Home Loan

[N][T][T][N][T]

An Essential Guide to Refinancing a Home Loan2024-04-22 | 5 Min

cibil Cibil

[N][T][T][N][T]

What Factors Do Not Affect Credit Scores?2024-02-28 | 7 min

home+loan Home Loan

[N][T][T][N][T]

Tips to Secure Quick Home Loan Approval2025-03-03 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Loan Against Residential Property: A Smart Financing Solution2025-03-10 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Loan Against Agricultural Land: Unlock the Value of Your Property2025-03-07 | 6 min

cibil Cibil

[N][T][T][N][T]

Know How Mortgage Loan Affect Your CIBIL Score2024-02-05 | 5 Min

loan+against+property Loan Against Property

[N][T][T][N][T]

Understanding the Fees and Charges on Your Loan Against Property2024-04-10 | 6 min

cibil Cibil

[N][T][T][N][T]

What are the Types CIBIL Errors & How to Correct Them?2023-11-22 | 6 min

home+loan Home Loan

[N][T][T][N][T]

Home Loans for Salaried Employees: Eligibility, Documents, and Application Process2025-03-18 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Property Mortgage Loan: A Smart Financing Option for Businesses2025-03-10 | 3 min

home+loan Home Loan

[N][T][T][N][T]

How to Calculate Your Home Loan Eligibility2025-03-05 | 3 min

[N][T][T][N][T]

Loan Against a Shop- Commercial Property Loans2024-12-18 | 2 min

home+loan Home Loan

[N][T][T][N][T]

Benefits of a Home Loan2023-02-20 | 4 min

loan+against+property Loan Against Property

[N][T][T][N][T]

3 Different Loan Against Property Types You Should Know About2024-02-13 | 5 Min

[N][T][T][N][T]

Home Loan for Pensioners: Eligibility and Benefits2025-03-11 | 3 min

home+loan Home Loan

[N][T][T][N][T]

5 Great Ways Women Can Benefit from Taking a Housing Loan2024-01-16 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Home Loan for Self-Employed Individuals2025-03-03 | 2 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Why Professional Loans Against Property Are Financially Beneficial?2023-03-03 | 5 min

cibil Cibil

[N][T][T][N][T]

Reasons Why Your CIBIL Score Is Going Down2024-04-10 | 4 min

home+loan Home Loan

[N][T][T][N][T]

Reasons Why a Housing Loan Application May Be Rejected2024-02-14 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

6 Reasons Why Collateral Matters When Applying for a Loan Against Property2023-02-27 | 5 min

cibil Cibil

[N][T][T][N][T]

Five Reasons Why a Bad Credit Score Could Lead to Loan Rejection2024-01-22 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Home Loan Refinancing: What, Why, and Things to Remember2024-06-17 | 5 Min

cibil Cibil

[N][T][T][N][T]

Top 10 Reasons For Low CIBIL Score & How To Improve It2024-03-01 | 5 min

[N][T][T][N][T]

What is the Purpose of CIBIL Score?2023-03-25 | 4 min

home+loan Home Loan

[N][T][T][N][T]

Benefits of a Joint Home Loan with your Spouse2023-08-04 | 4 min

home+loan Home Loan

[N][T][T][N][T]

What is the Process to Get Your Home Loan Approved Fast with Bajaj Housing Finance?2024-02-15 | 6 min

cibil Cibil

[N][T][T][N][T]

What is the Procedure to Check your CIBIL Score Rating?2023-03-27 | 4 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Easy Ways to Pick the Right Loan Against Property Tenor2024-05-14 | 3 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Pay-off Your Debt with Bajaj Housing Finance Loan Against Property2024-02-14 | 5 min

cibil Cibil

[N][T][T][N][T]

Different Types of Credit Report Errors and How to Fix Them_WC2023-07-11 | 4 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Common Mistakes You Must Avoid Making When Applying for a Loan Against Property2023-02-09 | 5 min

cibil Cibil

[N][T][T][N][T]

Minimum CIBIL Score for Business Loans2023-04-17 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Making Financial Planning Easy with a Home Loan EMI Calculator2023-09-06 | 2 min

cibil Cibil

[N][T][T][N][T]

Reasons to Maintain a Positive Credit Profile and a High CIBIL Score2023-03-01 | 5 min

cibil Cibil

[N][T][T][N][T]

Will a Loan Settlement Ruin My CIBIL Score?2023-03-21 | 4 min

[N][T][T][N][T]

Loan Against Property or A Home Loan: Know What You Need2024-06-11 | 5 min

loan+against+property Loan Against Property

[N][T][T][N][T]

Why Loan Against Property Can be a Good Credit Option for a Startup Business?2023-12-22 | 5 Min

loan+against+property Loan Against Property

[N][T][T][N][T]

Top Benefits of Loan Against Property Over Collateral-free Loans2023-02-23 | 3 min

home+loan Home Loan

[N][T][T][N][T]

Taking a Home Loan to Buy a Property for Investment? Here Are 5 Points to Consider2023-04-17 | 5 min

home+loan Home Loan

[N][T][T][N][T]

4 Key Benefits of Home Loan Balance Transfer to Bajaj Housing Finance Limited2023-01-09 | 5 min

cibil Cibil

[N][T][T][N][T]

Is a Good CIBIL Score Mandatory for Home Loan Approval?2023-02-17 | 4 min

cibil Cibil

[N][T][T][N][T]

Why is a CIBIL Score Measured Between 300 and 900?2024-05-07 | 4 min

tax Tax

[N][T][T][N][T]

Income Tax Structure in New Regime: New Tax Exemption Limit 20252024-05-08 | 4 min

tax Tax

[N][T][T][N][T]

8 Useful Income Tax Exemptions for Salaried Employees2024-04-18 | 7 min

home+loan Home Loan

[N][T][T][N][T]

What Affects the Interest Rate on Your Home Loan2024-03-13 | 5 min

home+loan Home Loan

[N][T][T][N][T]

Importance of an NOC Letter after Closing Your Home Loan2023-12-14 | 6 min

home+loan Home Loan

[N][T][T][N][T]

The Importance of a Home Loan NOC2023-01-31 | 7 min

home+loan Home Loan

[N][T][T][N][T]

Importance Of a Good Credit Score in The Home Loan Process2023-03-20 | 4 min

home+loan Home Loan

[N][T][T][N][T]

6 Ways to Reduce Your Home Loan Interest2024-03-20 | 4 min

loan+against+property Loan Against Property

[N][T][T][N][T]

How to Apply for a Mortgage Loan?2025-03-05 | 3 min

cibil Cibil

[N][T][T][N][T]

What Does a Zero or Negative Credit Score Mean?2023-02-24 | 4 min

cibil Cibil

[N][T][T][N][T]

Here Is How a Bounced Cheque Can Affect Your CIBIL Score2023-06-06 | 5 min

[N][T][T][N][T]

What are Tranche Disbursement and Tranche EMI in Home Loans?